Blog Post

Procurement Monthly: July 2026

Written

August 3, 2026

by

Dallán

Blog Post

Procurement Monthly: July 2026

Written

August 3, 2026

by

Dallán

Blog Post

Procurement Monthly: July 2026

.webp)

A call to initiate the break clause in Palantir's £330m NHS Federated Data Platform contract follows a wider conversation happening across the UK public sector tech procurement space, where calls are being made to prioritise business with British suppliers, small and medium-sized enterprises (SME), and to ensure social value is at the top of the agenda.

For suppliers, this creates significant commercial opportunity in surrounding work (transition, integration, data services), trust and ICB-level analytics buying, and the next wave of NHS contract renewals for data services worth hundreds of millions of pounds.

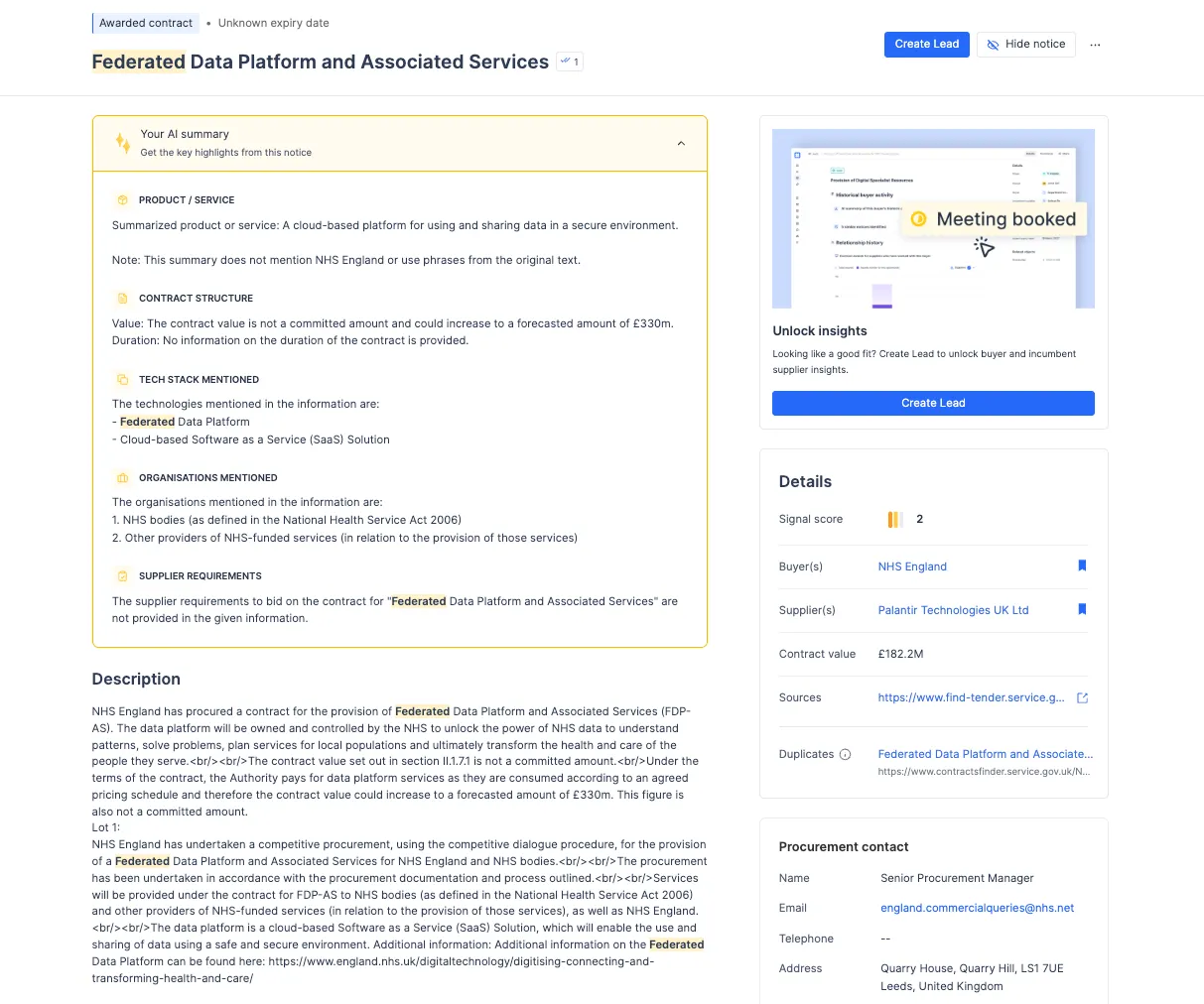

Ministers are reportedly considering a break clause in Palantir's £330m NHS Federated Data Platform (FDP) contract, with the deal potentially ending early if other suppliers can deliver the same outcomes. The contract was awarded in November 2023 to a Palantir-led consortium alongside Accenture, PwC, NECS and Carnall Farrar, and runs to 2030.

The published award value to Palantir Technologies UK Ltd on Stotles is £182.2m, with the £330m figure representing the maximum envelope as more trusts adopt the platform.

The FDP contract follows a 3+2+1+1 structure. This means it runs for an initial three-year term, followed by three possible extension periods. The first term ends in March 2027, and to continue beyond that point, the Department of Health and Social Care must actively choose to trigger the first extension. If it does not, the contract will naturally come to an end.

This makes 2026 a critical decision year. In the British Medical Journal, Health Minister Dr Zubir Ahmed said the government will decide “later this year” whether to trigger the 2027 extension. That decision will shape whether the NHS continues with Palantir, renegotiates its position, or prepares for a managed exit.

The controversy around Palantir’s NHS Federated Data Platform is not just about performance. It is about trust, value, and control.

Some NHS users say the platform is improving. Others reportedly find it difficult to use and question whether it is delivering enough value across the system. Those concerns sit alongside a bigger fear: lock-in. MPs have warned that the current subscription model could leave the NHS with no lasting software, intellectual property, or internal capability once the contract ends, despite more than £330 million being committed.

Palantir’s wider reputation adds fuel to the debate. Its work with defence, surveillance, and US immigration enforcement has made parts of the NHS, Parliament, and the public wary of giving the company such a sensitive role in national health data infrastructure. Supporters argue that using the 2027 break clause could cause disruption. Critics argue that disruption can be managed, and that short-term inconvenience should not become a reason to accept long-term dependency.

Palantir’s UK leadership has also pushed back strongly against calls to use the break clause. Louis Mosley, Palantir’s UK executive vice-chair, has argued that opposition is driven in part by dislike of Palantir’s US leadership and wider reputation, rather than the FDP’s performance in the NHS.

NHS England has awarded Imperial College Projects a £700,000 contract to evaluate the Federated Data Platform and assess whether it is meeting its objectives, delivering value for money, and creating measurable impact across the health system.

The review is expected to run from March 2026 to 2029, which creates an awkward timeline. The FDP’s break clause could be triggered in early 2027, well before the full evaluation is complete. That means any decision on whether to continue with Palantir, renegotiate, or start planning an exit will likely depend on early evidence around adoption, usability, operational value, and trust-level impact.

This matters because adoption remains uneven. Many trusts are still pushing back, some say their existing local systems already work well, and only part of the NHS is actively reporting benefits. Against that backdrop, the Imperial evaluation may become more than a neutral review. It could become a key battleground in deciding whether the NHS doubles down on the FDP, reshapes the contract, or prepares for life after Palantir.

This decision goes beyond a single contract. The government is now openly questioning whether a single overseas platform should sit at the centre of NHS data, and whether the FDP is delivering enough value to justify staying the course.

A wobble at the top of the NHS data stack could reshape buying behaviour across trusts, Integrated Care Boards, and adjacent departments over the next two to three years. If the NHS continues with Palantir, buyers may prioritise integration, adoption, and optimisation around the FDP. If the government steps back, renegotiates, or prepares to exit, the market could open up to alternative platforms, specialist data tools, and suppliers that can help local systems maintain control while still delivering national visibility.

When a major incumbent comes under pressure on a flagship contract, the work doesn't disappear; it gets redistributed. We are seeing a similar pattern in the Post Office Horizon scandal, where Fujitsu’s large and controversial contract is coming to an end, and suppliers like IBM are looking to win the business. The same logic applies to the FDP. The NHS still needs to integrate operational data, hit elective recovery targets, and run population health analytics. None of that stops while ministers debate the future of the prime contract.

Three things tend to happen in these moments.

First: The surrounding work expands. Even if the FDP stays in place, more spend is likely to flow into the services around it: data quality, local interoperability, transition readiness, exit planning, integration engines, and the analytics layers that sit above any platform.

Stotles data already shows this pattern. Alongside the headline £182.2m FDP award, NHS England and Arden & GEM CSU have signed surrounding contracts, including a £24.9m Foundry Transition and Exit Contract, an £11.5m Data Platform Services extension, and a £23.5m Data Management Platform Services contract. The FDP is already a multi-supplier ecosystem, not a single deal.

Second: Trust and ICB-level buying become more assertive. The FDP was always meant to be adopted trust by trust. If confidence at the centre weakens, local buyers may move faster on their own analytics, EPR integration, data modelling, and population health tools rather than wait for a national decision.

That shift is already visible. Across the NHS data, intelligence, and AI category, 150 contracts worth nearly £400m are set to expire in the next two years, covering areas such as regulatory intelligence, data modelling, and data safe haven work. These are exactly the spaces where suppliers can start positioning now. Source: Stotles NHS emerging tech contracts procurement 2025 report.)

Third: Decisions face tougher scrutiny. Under the Procurement Act 2023, which went live on 24 February 2025, contracts above £5m carry mandatory KPIs that must be tracked and published. The Act also introduces a central debarment register and tighter transparency requirements.

That means whatever happens to the FDP will happen in public, in detail. For challengers, that creates opportunity. For incumbents relying on opacity to stay embedded, it raises the stakes.

The government is signalling a clear shift in preference toward UK and SME suppliers, and away from over-reliance on large overseas tech platforms. The Procurement Act 2023 mandates that authorities identify and remove barriers to SME participation under Section 12, requires social value to weigh in tender decisions, and pushes for more competitive, flexible procedures over rigid multi-year direct awards. Combined with the FDP debate, the direction of travel is hard to miss.

Look at the numbers. According to Stotles' July 2025 report, Win in the growing £47bn digital government market, UK public sector technology spend reached over £47 billion across central government and local authorities between 2022 and 2025, with £19.4 billion of that flowing into data, AI and automation alone. NHS England sits among the top three central government data buyers, with a spend of £1.7 billion.

For suppliers, the read is straightforward. If you're a UK-headquartered data, AI or interoperability vendor, you're operating in a more favourable political climate than UK suppliers have had in some time. If you're an overseas platform, you need a sharper UK delivery story, a stronger local partner ecosystem, and clearer social value commitments to stay competitive.

Three groups of suppliers stand to gain commercially. None of them have to wait for a final decision to start positioning.

No single supplier replaces Palantir overnight. The FDP is technically embedded across acute trusts, and migration is a multi-year effort with real cost. The surrounding spend, the renewals, and the next wave of trust-level analytics are absolutely up for grabs.

Published notices rarely show the full shape of how a major supplier relationship actually develops. Consortium structures, direct awards, pilots, FOI responses, partnership announcements and redacted contracts all sit underneath the headline.

Our earlier Palantir analysis walked through exactly how this plays out. Worth reading alongside this piece if you want the deeper view on consortium structures and document trails.

For this story, the takeaway is simpler. If you're tracking the FDP situation through notice headlines alone, you're missing the framework call-offs, surrounding contracts, FOIs, pilots and partner ecosystem where most of the commercial detail actually sits.

Three moves, in order of urgency.

1. Map the FDP-adjacent contracts already in market. Transition, exit, data services and integration work is being signed today, and you can see it on Stotles. Look at NHS England's recent activity, plus the major NHS CSUs (Arden & GEM, NECS, SCW). These are the contracts that grow regardless of what happens to the prime.

2. Get closer to ICBs and trusts now, not in 2027. The 42 ICBs vary massively in digital maturity, with some sitting on substantial unspent IT capital. North Central London ICB alone allocated £63.6m to IT projects in 2024/25 (Source: Stotles Integrated Care Systems reveal 2024/2025 budgets report). Trust-level buyers move faster than the centre and are more open to challenger suppliers, particularly under the Procurement Act's pre-market engagement provisions.

3. Position your social value and UK delivery story explicitly. Under the Procurement Act, social value, sustainability and SME inclusion now weigh meaningfully in evaluation. If you're a UK supplier, lean into that. If you're an overseas vendor, build the partner ecosystem that lets you compete on those terms.

The Palantir FDP story isn't really about Palantir. It's about a government pushing harder on transparency, social value and UK supplier inclusion, while also recognising that buying a platform isn't the same as fixing the data problem underneath it.

Suppliers who win in this market over the next three years won't be the ones reacting to the next news cycle. They'll be the ones already mapped to the surrounding spend, already engaged with ICBs and trusts, and already positioned for a procurement regime that's tilting toward challengers. The window is open now. It won't stay that way once the FDP question is settled.

The Federated Data Platform contract was awarded to a Palantir-led consortium in November 2023 and is valued at up to £330 million over seven years as more trusts adopt the platform. The published award value to Palantir Technologies UK Ltd on Stotles is £182.2m, with surrounding contracts adding tens of millions more.

The reasoning combines political appetite for UK-led tech, concerns about over-reliance on a single overseas platform, and questions about whether the FDP is delivering enough operational value across NHS trusts to justify continuing as planned. The Procurement Act 2023 has also raised the bar on transparency and supplier performance tracking.

Direct competitors in NHS data and analytics include Accenture, IBM, BJSS, Aire Logic, Hitachi Solutions and PA Consulting. In the wider government data, AI and automation category, AWS, Snowflake, Capgemini and Deloitte are major incumbents. Specialist UK-headquartered analytics and interoperability vendors are increasingly well placed under the Procurement Act 2023.

Suppliers can monitor expiring contracts, pre-tender notices and pipeline notices through procurement intelligence tools that aggregate published notices, framework activity, FOI responses and supporting documents. Across the NHS data, intelligence and AI category alone, 175 contracts worth £388m are due to expire in the next two years.

The Procurement Act 2023 went live on 24 February 2025 and reshaped UK public procurement around transparency, SME inclusion, social value and supplier performance tracking. It introduced 17 new notice types, mandatory KPIs on contracts above £5m, a centralised debarment register, and Section 12 obligations to remove barriers to SME participation, all of which favour challenger suppliers.