Digital Outcomes 6: Insights for a winning strategy

Written

January 30, 2025

by

Dallán

Digital Outcomes 6: Insights for a winning strategy

Written

January 30, 2025

by

Dallán

.jpg)

Released on 21 June 2025, the UK government's 10-Year Infrastructure Strategy represents a comprehensive and unprecedented shift in how the country approaches infrastructure planning, funding, and delivery. For the first time, it takes into consideration:

The 10-Year Infrastructure Strategy introduces a new player. The National Infrastructure and Service Transformation Authority (NISTA) was formed to centralise infrastructure expertise, ensure project deliverability, and guide procurement excellence across the UK.

The strategy is backed by at least £725 billion in funding over the next decade. It includes a soon-to-be-launched online Infrastructure Pipeline to provide visibility into upcoming opportunities for industry.

By the end of this report, you will have the tools to:

The UK government is committing to at least £725 billion in infrastructure funding over the next decade, representing one of the most significant infrastructure investments in British history.

Funding will be inflation-indexed beyond 2029-30 and structured with long-term commitments. For example, £20B for school rebuilding by 2035, £70B for healthcare infrastructure by 2030, and £7.9B for flood defences to 2036.

What this means for suppliers: More reliable commercial forecasting, smoother pipeline planning, and justification to scale local operations.

The government is revamping procurement by eliminating rigid benefit-cost thresholds (e.g., BCR filters) in favour of place-based outcomes, providing stronger compliance with the Construction Playbook, and making a push toward social value procurement. This includes upcoming consultations on rules to favour bidders who create high-quality jobs, provide skills training, and promote SME involvement.

Why it matters: Suppliers with strong local employment stories, innovation credentials, or digital delivery capabilities will be at a competitive advantage.

Launching in July 2025, the online Infrastructure Pipeline will provide 10-year forward visibility into public and major private infrastructure projects, including details on timelines, budgets, procurement routes, and funding statuses, as well as geographic segmentation for regional targeting.

Why it matters: This eliminates traditional opacity in public sector work, enabling strategic bid planning at both national and regional levels.

With Public-Private Partnerships (PPPs) back on the table, and £59B in new financial transaction capacity via public investment vehicles (e.g., National Housing Bank, Great British Energy), the government is building co-funded models (e.g., RAB for Lower Thames Crossing, Sizewell C) and offering new PPP pilots in community healthcare, primary care, and public estate decarbonisation.

Why this matters: Suppliers with commercial structuring, investment, or long-term maintenance models can partner in ways that go far beyond traditional construction contracts.

The report provides a breakdown of 7 key focus areas with clear, funded commitments across every major infrastructure vertical:

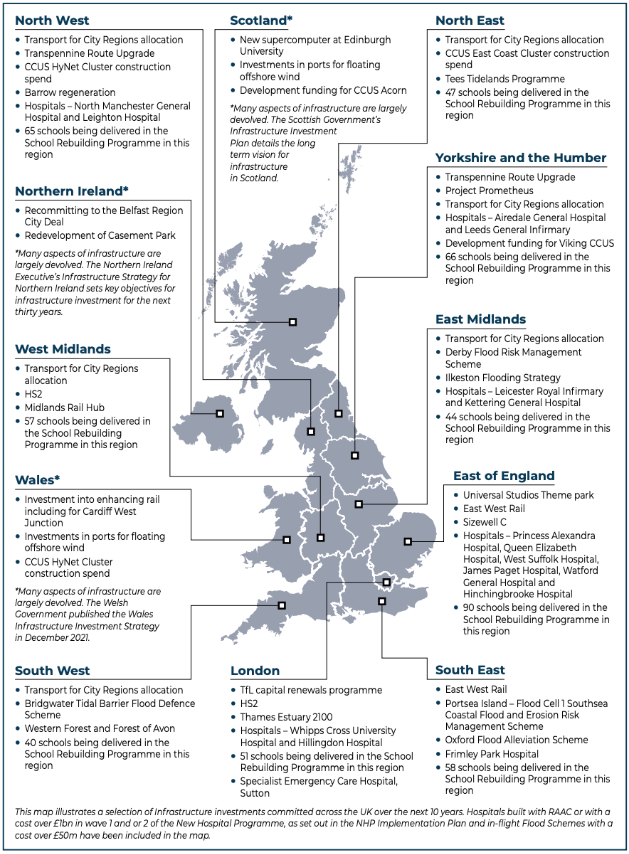

The report highlighted 12 regions where investment will be allocated, enabling suppliers to geo-target business development opportunities based on forecasted spending. These include:

Procurement will increasingly bundle complementary needs (e.g., housing + water + roads), via place-based business cases. In addition, NISTA’s spatial digital tool will provide visibility into cross-sector infrastructure needs for areas such as the Oxford-Cambridge region or West Yorkshire.

So what? Bidders will need to design interoperable, multi-disciplinary solutions. Teams that combine civil, digital, and environmental expertise will be more competitive.

Over the past three years, the UK public sector construction market has demonstrated sustained growth in both the value and volume of awarded contracts, signalling expanding opportunities for suppliers. In the most recent 12-month period (2024–2025), total awarded contract value reached £53.64 billion across 14.5k contracts.

Construction spend in the public sector has grown over the past three years.

The awarded contract value is up by more than £11 billion since 2022–2023. That’s a 26% increase, with a strong average growth rate of 12.4% per year. This reflects long-term government investment across key areas like transport, defence, healthcare and education.

Volume has also grown, but not as quickly.

Contracts jumped by 12.7% in 2023–2024, but growth flattened this past year. While the number of awards stayed steady, spending went up. That tells us contract values are getting bigger. We're seeing more bundling, longer-term commitments and larger awards through central frameworks.

The live pipeline is broad, covering key verticals with clear investment priorities.

As of 14 July 2025, local government leads in volume of live opportunities, with 1,053 live opportunities worth £33.9 billion.

Regional infrastructure, highways, and place-based development drive this. Central Government, which includes defence, accounts for £29.3 billion across 329 contracts. These are typically higher-value, national-scale projects aligned with major infrastructure programmes and estate modernisation.

Healthcare remains an active delivery area, with £6.1 billion across 105 contracts. This reflects continued investment in NHS facilities and community health infrastructure. Education and Blue Light Services each contribute a smaller number of contracts, but represent targeted capital upgrades for schools, police, and fire departments.

Meanwhile, housing associations (grouped under “Other”) account for £10.3 billion in value across 390 contracts. This shows strong activity in affordable housing, decarbonisation, and retrofit works.

The top five buyers reflect where the government is placing long-term capital. Defence and transport lead on spend, with MOD and National Highways consistently awarding high-value, multi-year contracts.

The Home Office ranks third by value despite a relatively low contract count, showing a focus on large, complex estates and security infrastructure. Education and rail continue to feature prominently through school rebuilding and megaprojects like HS2.

These suppliers are among the most embedded across public infrastructure delivery. WSP leads on both volume and value, underlining its position across planning, engineering, and project management.

Aecom and Arup have similar contract volumes but focus more on consultancy and technical support, which is reflected in their lower aggregate values. Jacobs and AtkinsRéalis both show a strong balance between volume and strategic delivery, securing roles in major frameworks and long-term capital programmes.

These three frameworks shown below are the most active procurement frameworks routes over the past year. Construction Professional Services remains heavily used across early-stage design, engineering, and project management.

Offsite Construction Solutions stands out for its value, showing how public buyers are scaling modular delivery in schools, healthcare, and housing. Planned Maintenance and R&M Works are being used for essential upgrade works, especially by local authorities and housing associations.

Identifying opportunities in public sector construction requires a different approach than in categories like technology or facilities management, where contract expirations often signal clear buyer intent.

For construction firms, the path to growth in the public sector is less about tracking renewals and more about understanding strategic capital programmes, pipeline visibility, and early-stage project planning.

Below are five practical recommendations for construction companies aiming to expand their footprint across the UK public sector.

1. Target high-growth and reform-focused areas

Construction suppliers should focus their efforts on mayoral combined authorities, which are gaining greater control over local infrastructure funding and delivery. Priority should be given to transport, education, and healthcare projects highlighted in the National Infrastructure Pipeline. Early-stage engagement is essential for securing roles in major strategic programmes such as HS2, Sizewell C, and East West Rail, where long-term delivery and supply chain planning are already underway.

2. Strengthen positioning on social value

With public sector procurement increasingly shaped by social value mandates, construction firms must align their offerings to support UK skills development, SME participation, and the net-zero transition. Competitive bids will demonstrate commitments to local job creation, training programmes, and decarbonisation, reflecting the government’s emphasis on inclusive and sustainable growth.

3. Monitor NISTA and pipeline updates

The upcoming Digital Infrastructure Pipeline (due July 2025) will be a key tool for identifying early-stage opportunities, particularly in emerging sectors. Suppliers should ensure they are pre-qualified, proficient with procurement platforms, and actively monitor communications from NISTA (National Infrastructure and Spatial Transformation Authority) to stay ahead of project announcements and funding shifts.

4. Explore new commercial models

As infrastructure financing evolves, suppliers should explore Public-Private Partnership (PPP) opportunities, in particular where long-term revenue streams exist, such as in transportation, energy, and utilities. It is also crucial to understand the role of new funding institutions, including the National Housing Bank, the National Wealth Fund, and Great British Energy, which will enable blended finance for more complex infrastructure delivery.

5. Prioritise digital and environmental readiness

Demand is rising in sectors such as data centres, EV infrastructure, flood resilience, and sustainable construction. To stay competitive, firms should offer digitally enabled planning, delivery, and asset management solutions. This will ensure alignment with NISTA’s spatial data platforms and the UK’s broader digital transformation agenda for infrastructure.

The UK’s 10-Year Infrastructure Strategy opens up a £725 billion commercial opportunity, but winning requires more than just showing up. Stotles gives suppliers the tools to act early, engage the right buyers, and win more business. From surfacing strategic pipeline opportunities to tracking high-value frameworks and expiries, Stotles connects your team to the insights that matter.

If you’re serious about growing in public sector construction, now is the time to move. Get in touch with the Stotles team to build your go-to-market plan and get ahead of the competition.

Enter your details to download this report.

Enter your details to download this report.