The Local Government supplier handbook

Written

February 26, 2024

by

Xavier Garnham

The Local Government supplier handbook

Written

February 26, 2024

by

Xavier Garnham

.png)

The NHS has begun to roll out its 2025/2026 Joint Capital Resource Use Plans (JCRUPs) for Integrated Care Boards (ICBs). These are the types of buyer signals the top suppliers monitor that make or break public sector sales strategies.

We’ve identified £6.3b in confirmed funding across 32 of the 42 published plans. It includes:

This report breaks down the capital plans sourced directly from official ICB publications so you don't have to. It includes:

As with previous years, some ICB plans have yet to be published. Where gaps remain, those boards are excluded from this analysis, but we’ll continue to update our data as new information becomes available.

Access our Google Sheet for a detailed breakdown of Integrated Care Board funding. It includes the full 2025/26 allocation, year-on-year changes, totals for technology, infrastructure and equipment, and confirmed named projects for each ICB.

The 2025/26 capital plans show strong upward momentum across most NHS regions, with notable growth in the Midlands (£1.3b), North East & Yorkshire (£1.3b), and London (£1b), together accounting for the bulk of new spend.

The South West (£574.7m) was the only region to see a contraction, reflecting shifts in national funding priorities and project phasing.

Full table of 32 ICBs (by clicking on the ICB name, you can visit the buyer profile on the Stotles platform to dive deeper into the JCRUP, procurement activity, top suppliers they are working with and key contacts controlling budgets).

There are three core areas where the ICBs are showing promise for suppliers to align with their priorities. These are IT and digital, infrastructure and construction, and equipment and machinery.

For suppliers, focusing on ICBs with rising capital allocations can unlock the strongest opportunities.

In 2025/2026, 17 ICBs reported year-on-year growth in their capital budgets, with several showing double-digit increases.

Below, we highlight the top ICBs tanked by percentage change YoY.

West Yorkshire is a standout growth region in 2025/26, with capital funding up 34.7% to £450.6m.

Investment is spread across digital (£19.3m), infrastructure (£224m), and equipment (£11m), offering suppliers opportunities in digital health, estates, and clinical assets.

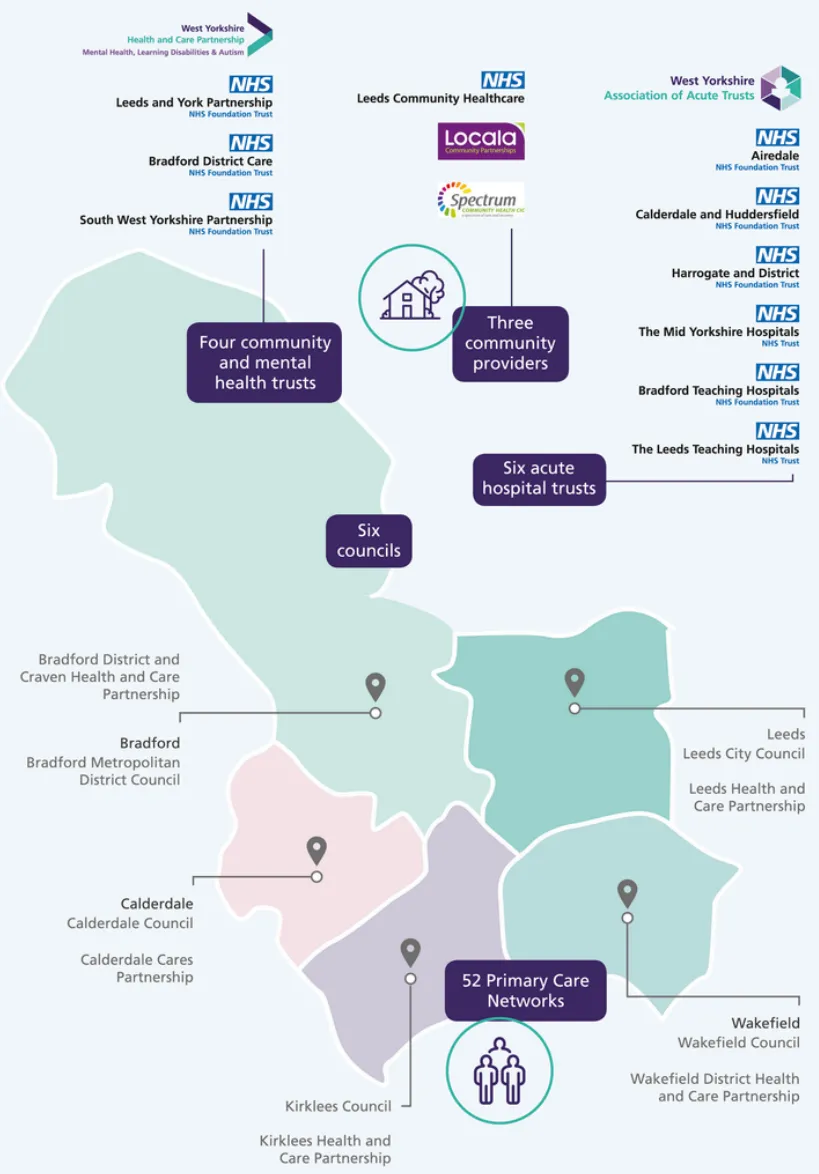

Below is a map of the NHS organisations that fall under West Yorkshire ICB.

The system also carries a heavy £862m backlog, of which £590m is critical (notably Airedale RAAC and Leeds Teaching Hospitals), driving demand for safety works and new build schemes.

While cash pressures, inflation, and IFRS16 accounting pose delivery risks, the ICB’s strong capital envelope and push on Net Zero create clear entry points for suppliers across construction, digital, equipment, and sustainability solutions.

Based on funding allocation and where West Yorkshire's priorities are focused, these hotspots present the best opportunities for suppliers.

Not all ICBs are seeing growth in 2025/2026.

This year, 13 ICBs reported year-on-year reductions in their capital budgets, with some experiencing double-digit declines. These cuts highlight regions where funding is tightening and where procurement opportunities will be more limited and focused on essential projects only.

Below, we spotlight the ICBs with the largest budget reductions for 2025/26, showing both the net and percentage change compared to the previous year.

Devon has seen the sharpest budget decline in 2025/26, with capital funding down 45% from £200.1m to £109.8m.

Despite the cut, it remains one of the most transparent systems in funding allocation, with substantial allocations across technology (£55.8m for EPRs, cyber upgrades, digital replacements), infrastructure (£49.6m for radiotherapy, UEC, SDEC and CDC schemes), and equipment (£57.4m for LINAC, MRI, and diagnostics).

Below is a map of the NHS organisations that fall under Devon ICB.

Funding pressures mean many bids (~£114m+) outstrip allocations, forcing deferrals of urgent schemes such as nuclear medicine, renal dialysis, and pathology upgrades.

Significant backlog risks (£84m at RDUH; £22.5m at DPT), lease commitments overshooting allocations by £32m, and inflationary cost pressures compound the challenge.

Based on funding allocation and where West Yorkshire's priorities are focused, these hotspots present the best opportunities for suppliers.

1. Dive deeper into ICB capital plans

2. Explore competitor activity

3. Map routes to market most used by the NHS

4. Track regions under funding pressure

5. Identify strategy partnership opportunities

These are five recommendation to get moving quickly using the ICB JCRUPs. For more advice on how to build a successful NHS strategy, reach out to one of our team to learn more.

There is £6.3b in confirmed capital for 2025/26 live across 32 ICBs.

Now is the moment to be proactive and set a clear plan to build pipeline while your competitors are still figuring out their NHS strategy.

What to do now:

Keep up to date with the most recent updates on the Stotles platform and set yourself up for success.

Enter your details to download this report.

Enter your details to download this report.